Science Based Targets (SBTi)

You might have heard of Science Based Targets to achieve Net Zero, but what does it mean exactly?

The Paris Agreement’s stated goal is ‘to limit global warming to well below 2, preferably to 1.5 degrees Celsius, compared to pre-industrial levels’.

Science-based targets provide a clearly-defined path in line with the latest climate science to reduce emissions in line with the Paris Agreement goals.

The Science Based Targets initiative (SBTi) is a partnership between CDP, World Resources Institute (WRI), the World Wide Fund for Nature (WWF), and the United Nations Global Compact (UN Global Compact). The SBTi call to action is one of the We Mean Business Coalition commitments.

The aim is to drive positive climate action in the private sector by helping them establish science-based targets to Net Zero. Through SBTi, private companies can set validated near and long-term science-based Net Zero targets consistent with limiting temperature rise to 1.5°C to help drive the global transition to net-zero.

SBTi targets have now become the globally accepted standard for companies to create actionable plans for carbon reduction and Net Zero targets.

What do short-term and long-term targets mean?

As per SBTI:

‘Near-term targets must cover a minimum of 5 years and a maximum of 10 years from the date the target is submitted to the SBTi for official validation. Long-term (net-zero) targets shall have a target year no later than 2050.’

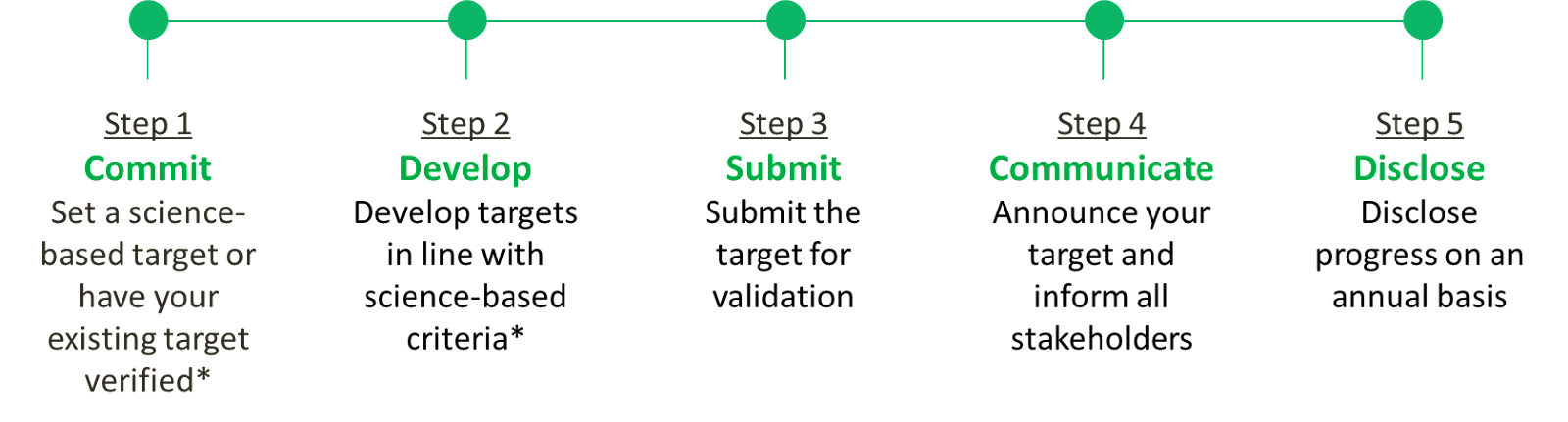

What does the process look like?

However, the process and costs are very different for SMEs.

The process for SMEs

SBTi has made this process slightly easier for SMEs.

SMEs can bypass the initial two steps of committing to set a target and getting it validated. They can instead move on to immediately setting near-term science based targets for Scope 1 and 2 emissions, and optionally, also Net Zero targets by choosing from one of several already predefined target options.

SMEs also have a significantly lower costing for setting targets. Further SMEs with HQs in developing countries and economies in transitions also have the option to request a waiver for their target submission fees - more details below.

What are the target options for SMEs?

As SBTi states it, following are the target options for SMEs:

Near-term targets - absolute Scope 1 and 2 GHG emissions reduction targets to be achieved by 2030, from a predefined base year

Net-zero targets* include:

Long-term science-based targets which are absolute scope 1, 2 and 3 GHG emissions reduction targets that should be achieved by 2050, from a predefined base year.

A commitment to neutralise any unabated emissions when the long-term science-based target is achieved.

What is the definition of a SME?

SBTi defines an SME as an independent, non-subsidiary company with fewer than 500 employees. 500 employees means headcount and not FTE. If the size of your organisation fluctuates, then it is advised to use an average headcount number.

Note that this definition does not include Financial Institutions (FIs) and Oil & Gas companies.

What other guidelines do SMEs need to keep in mind?

For setting up a near-term science based target, SMEs need to achieve the target in accordance with the rules of Greenhouse Gas (GHG) Protocol in the specific timeframe.

For Scope 1 and 2 emissions, SMEs need to publicly report their company-wide Scope 1 and Scope 2 GHG emissions inventory and progress against published targets on an annual basis. Companies have to follow GHG Protocol Corporate Accounting and Reporting Standard and Scope 2 Guidance.

While SBTi does not have a requirement to specific near-term Scope 3 targets to be set by SMEs, it encourages companies to to familiarise themselves with SBTi Criteria and Target Validation Protocol and also measure and reduce Scope 3 emissions following GHG Protocol Scope 3 Accounting and Reporting Standard.

There are also different targets if SMEs decide to adopt the optional Net Zero targets.

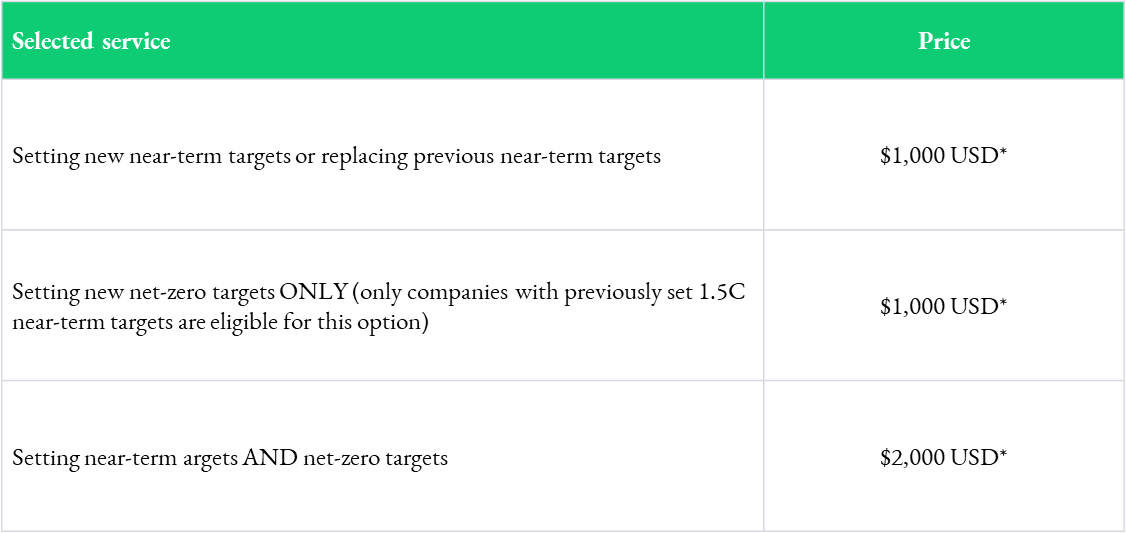

What are the costs for SMEs?

SMEs have significantly lower fees compared to standard fees of USD 9,500 and up (+VAT).

Further, SMEs that have HQs in developing countries and economies in transition also have the option to request a waiver for their target submission fees. More details on how these countries are defined can be found in Table B and C on pages 141/142 here - United Nations Secretariat’s Department of Economic and Social Affairs.